According to Worldpanel’s beauty panel data, demand for beauty products in China remains strong but purchasing decisions are becoming increasingly refined and complex. In this new and highly competitive landscape, brands can achieve differentiation through precise positioning and innovative breakthroughs.

There are five key opportunities in China’s beauty market for 2025, which we’ve summarised using the acronym FOCUS.

F (Fragmentation of Demands)

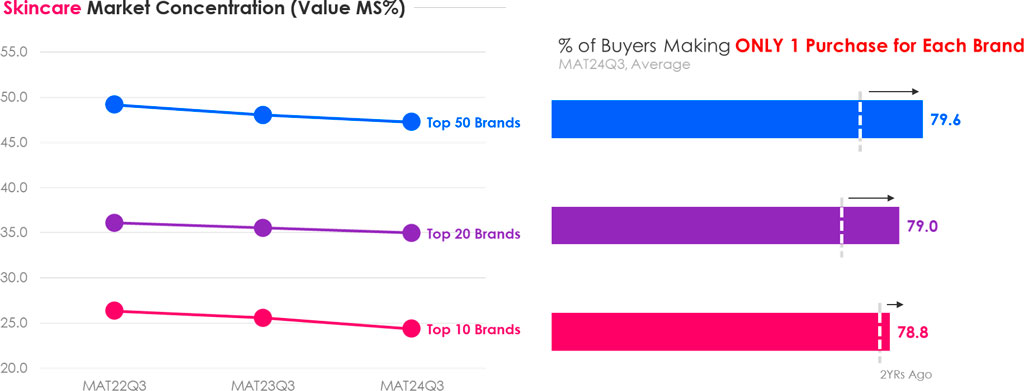

The beauty market is experiencing a transformation in consumer behaviour. In skincare, leading brands are losing their dominance, and consumers are purchasing leading brands far less frequently. This indicates that brand loyalty is continuously decreasing.

Source: Kantar Worldpanel, Individual Beauty Panel, Tier 1-5 & Ages 15-64.

Consumers are showing increasing openness to exploring diversified niche brands, rather than sticking to a single brand to meet their varied beauty needs. They pay more attention to how well products match their personal needs rather than blindly chasing big brands. They also value the actual usage experience products provide, over the price tag alone.

A rich brand matrix and category innovation are providing consumers with more choices, prompting increasingly rational and precise purchasing decisions.

Furthermore, beauty aspirations have extended beyond traditional skincare and makeup, evolving into the pursuit of comprehensive beauty care. Segments such as hair care and body care are showing strong growth. Concepts like ‘silky hair’, ‘healthy scalp with high cranial top’, and ‘elbow whitening’ are gaining traction on social media platforms.

The demand for comprehensive care not only creates differentiated market entry points for emerging brands, but also forces traditional big brands to accelerate product innovation and strategic transformation.

O (Occasion-based Demands)

Chinese consumers’ demands have shifted from single product functionality to precise solutions that are driven by specific scenarios.

For example, morning skincare emphasises anti-oxidation and sun protection, while evening skincare leans towards anti-aging and repair. Weekday skincare focuses on quick efficiency, while weekends are about all-around immersive care, from cleansing to masks and serums, and paired with home beauty devices to create a complete skincare ritual.

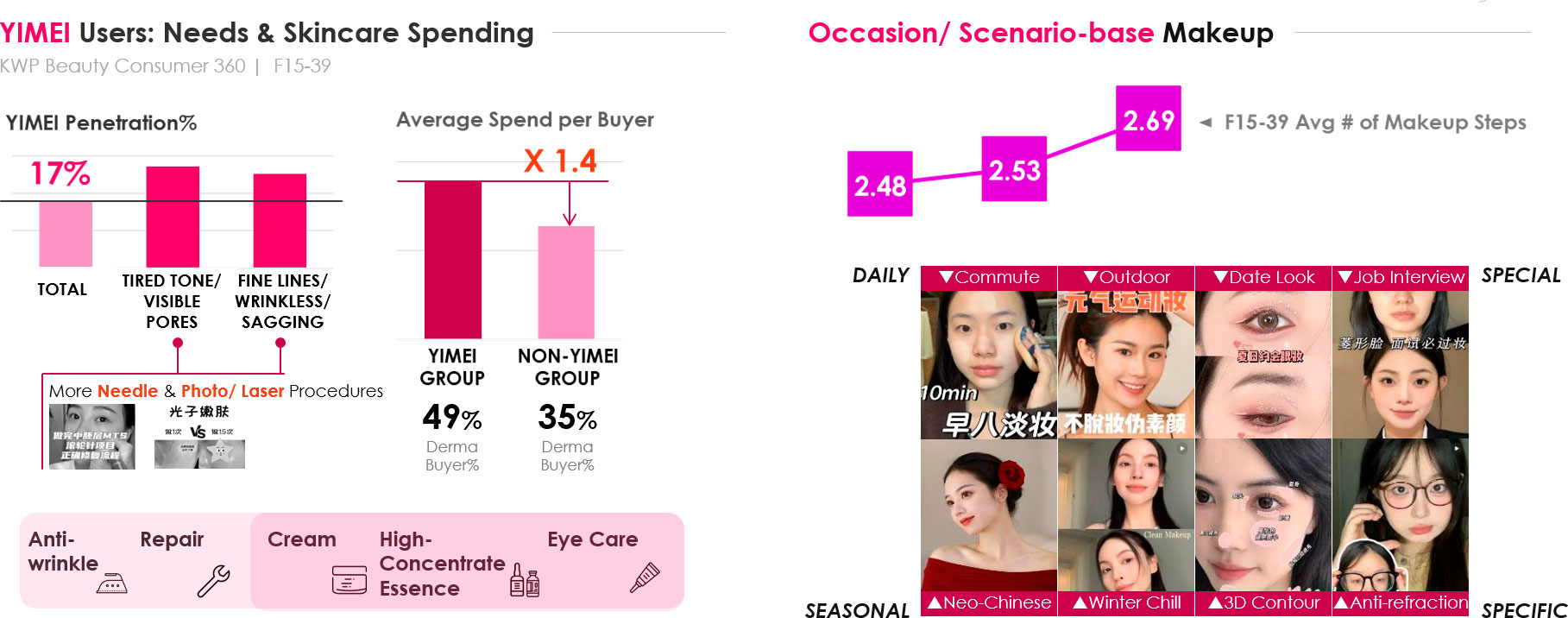

Additionally, the annual skincare expenditure of medical beauty users is approximately 1.4 times of others, showing a strong preference for restorative products, especially high-efficacy categories like creams and serums; continuing rise of medical beauty creates another opportunity for targeting occasion-based demands.

Source: Kantar Worldpanel, Individual Beauty Panel, Tier 1-5 & Ages 15-64.; KWP Beauty Consumer 360.

In the makeup sector, core consumers in the 15-39-year-old group are continuously refining the steps in their routine. Trends like ‘vibrant workout makeup’, ‘professional workplace makeup’, and ‘romantic date makeup’ reflect the strong demand for personalisation. More and more brands are exploring consumer pain points and emotional needs in different scenarios through precise product positioning and marketing strategies.

C (Convergence of Functions)

Consumers are shifting from demands for single efficacy products to an integrated skincare concept that aims to improve overall skin health from the root, while addressing specific issues. For instance, individuals with oily acne-prone skin are no longer only focused on oil control and acne removal, but also call for hydration to balance oil-water levels. In whitening, the consumer focus has shifted from simple brightening of the skin tone to creating a healthier “glow” from within using “rejuvenate” approach.

This trend of ‘multi-effect synergy’ has extended from facial care to body care, with gentle and safe formulas and sensitive skincare products becoming market favourites. Brands like Cetaphil and CeraVe, with their professional medical background, are combining moisturising, soothing, and repair functions through scientific formulations.

U (Underlying Demand Sophistication)

A deep understanding of the underlying logic behind Chinese consumers’ purchasing decisions is crucial. Brands need to go beyond basic skincare to capture the precise pain points of specific groups in specific life scenarios.

For example, YSL’s Night Reboot Serum focuses on ‘eliminating fatigue after overtime’ and ‘reviving dull skin after late nights’, directly addressing the pain points of urban white-collar workers and night owls.

Innovation in ingredients has become the core battleground for brand differentiation. Relying solely on ‘efficacy’ is no longer enough to stand out. Consumers are pursuing exclusive formulas, rare plant extracts, and patented technology upgrades, along with extremely high quality ingredients.

S (Storytelling for Emotional Resonance)

Brands face dual challenges: the homogenisation of product development, formulas, and core ingredients which makes technical differentiation difficult, and the diminishing influence traditional promotional activities have on consumer decisions. Creating emotional resonance between the brand and consumers has become the key to breaking through.

Take Proya for example. Its brand philosophy of ‘breaking gender bias and empowering women’ precisely aligns with contemporary women's desire to realise their self-value.

Emotional marketing strategies not only enhance the brand’s appeal but also build unique brand assets beyond product efficacy. The shift from functional consumption to emotional consumption drives brands towards deeper value creation.

In the rapidly evolving digital age of China’s beauty industry, constructing sustainable competitive advantages relies on deep, data-driven insights. Precisely capturing subtle changes in consumer needs is essential for brands to maintain relevance and vitality into the future.

Consult our Beauty Experts Join our webinar