Grocery price inflation has nudged down slightly to 5.0%, while take-home sales at the grocers grew by 4.0% over the four weeks to 10 August versus last year, according to our latest figures. The rate of grocery price inflation was 5.2% in July.

We’ve seen a marginal drop in grocery price inflation this month, but we’re still well past the point at which price rises really start to bite and consumers are continuing to adapt their behaviour to make ends meet. What people pay for their supermarket shopping often impacts their spending across other parts of the high street too, including their eating and drinking habits out of the home. Casual and fast service restaurants especially have seen a decline in visitors over the summer, with trips falling by 6% during the three months to mid-July 2025 – compared with last year. The outliers in this are coffee shops which have bucked the trend.”

Brands grow ahead of own label

While people are making savings outside of the home, they are still seeking treats in store. Sales of branded grocery items grew by 6.1% this month, putting them ahead of own-label alternatives which were up by 4.1% –the largest gap in favour of brands since March 2024. Branded sales make up 46.4% of all grocery spending but are particularly dominant in personal care, confectionery, hot drinks and soft drinks where they account for more than 75% of money through the tills. While a far smaller part of the market, premium own-label is also continuing to do well and sales rose by 11.5% this period.

There’s a significant milestone in the freezer aisles this year as the fish finger turns 70 in September. The humble fish finger remains as popular as ever and nearly one billion were sold in the past year, with more than half of households grabbing a box.

Their enduring presence on our plates reflects a much broader shift in people looking for easy and quick to prepare foods. The average home cook now spends three minutes less preparing the evening meal than they did in 2017 at just under 31 minutes.* We can see this trend in the growth of things like microwaveable rice, ready meals and chilled pizza too, which have grown by 8%, 6% and 5% respectively.

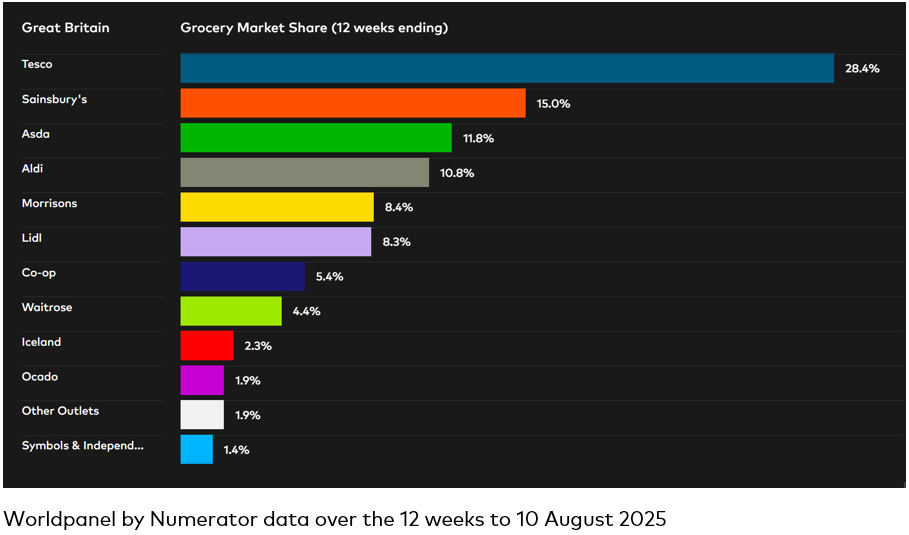

Lidl joins Ocado as fastest growing grocer

Lidl and Ocado were tied for top spot as the fastest growing grocers over the 12 weeks to 10 August 2025, with sales at both retailers up by 10.7% compared to the same period last year. Lidl’s share of the market increased by 0.5 percentage points to 8.3%, while Ocado now holds 1.9%, up from 1.8% in 2024. Online sales across all retailers rose by 6.7% over the 12 weeks.

Tesco enjoyed its largest monthly share gain since December 2024 as its hold of the market rose by 0.8 percentage points to 28.4%. This was driven by sales growth of 7.4% compared to last year.

Spending through the tills at Sainsbury’s was up 5.2% on last year, taking its portion of the market to 15.0%. Sales at Aldi were 4.8% higher, giving it a 10.8% share. Asda and Morrisons’ shares now stand at 11.8% and 8.4% respectively.

Spending at Waitrose grew by 4.8% over the 12 weeks, as its market share sits at 4.4%. With its sales rising by 3.4%, Iceland’s hold of the market remains at 2.3%. Convenience specialist Co-op has a 5.4% share of take-home sales.

*Worldpanel by Numerator Usage Foods, time taken to prepare evening meal 52 weeks ending June 2025 vs 52 weeks ending December 2017